How Compound Interest Works and Why It Matters for Your Future

Albert Einstein is often credited with calling compound interest the eighth wonder of the world. Whether or not he actually said it, the principle behind it is undeniable — understanding how compound interest works can be the difference between a comfortable retirement and a financially stressful one.

What Is Compound Interest?

Compound interest is the process by which interest is earned not only on your original investment but also on the interest that has already been added to it. Over time, this creates a snowball effect where your money grows at an accelerating pace.

This is different from simple interest, where you only earn interest on the original principal amount throughout the investment period.

How Compound Interest Works

Calculate While You Read

Free calculators related to this article — instant results, no signup.

When you invest a sum of money, interest is calculated and added to your principal at regular intervals — monthly, quarterly, or annually. In the next period, interest is calculated on this new, higher balance, which includes both your original investment and the interest already earned.

The longer your money stays invested, the more pronounced this compounding effect becomes, since each period builds on a progressively larger base.

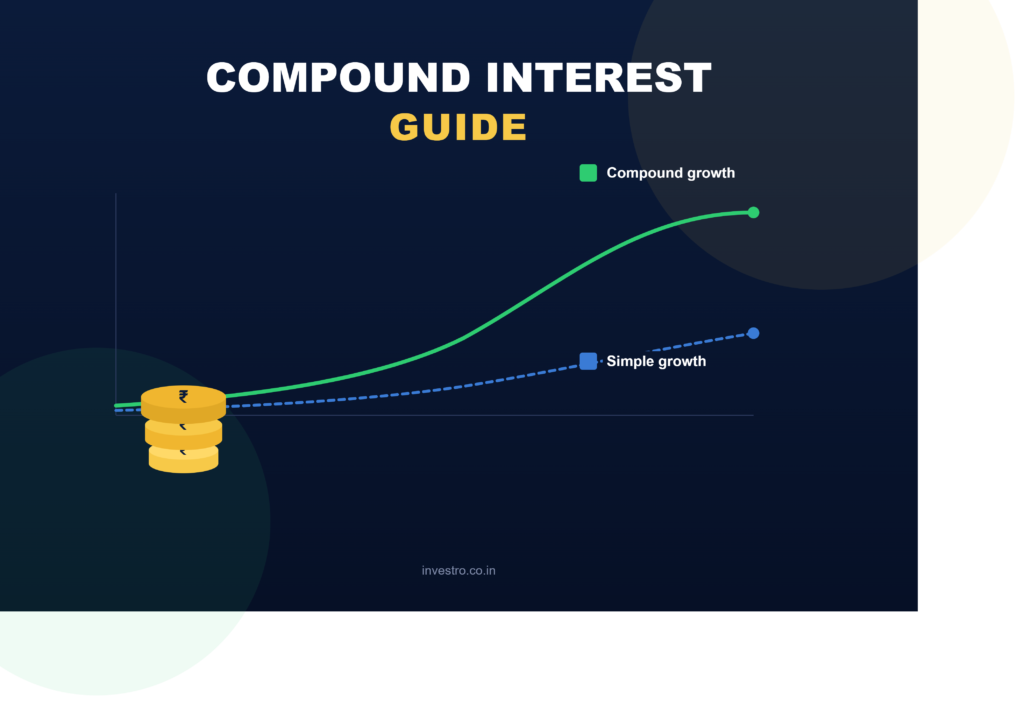

Compound Interest vs Simple Interest

Simple Interest

Simple interest is calculated only on the original principal amount. If you invest ₹1 lakh at 8 percent simple interest for 10 years, you earn ₹8,000 every year, totalling ₹80,000 in interest.

Compound Interest

With compound interest at the same rate, your interest is added back to the principal each year, so you earn interest on a growing amount. Over 10 years, this can result in significantly higher total returns compared to simple interest.

Key Factors That Affect Compounding

Time Period

Time is the most powerful factor in compounding. The longer your money remains invested, the more periods of compounding it experiences, leading to exponential rather than linear growth.

Rate of Return

A higher rate of return accelerates compounding significantly. Even a small difference in annual return can result in a substantially larger corpus over long periods.

Compounding Frequency

Interest can compound annually, semi-annually, quarterly, or monthly. More frequent compounding results in slightly higher overall returns, even at the same annual rate.

Where Compound Interest Applies

Mutual Fund SIPs

When you invest through a SIP, your returns are reinvested, allowing both your contributions and your earlier gains to generate further returns over time.

Public Provident Fund (PPF)

PPF compounds interest annually, and because of its long 15-year tenure, even modest yearly contributions can grow into a substantial corpus.

Fixed Deposits

Bank fixed deposits often offer compounding at quarterly intervals, allowing your interest to grow on top of previously earned interest before maturity.

The Power of Starting Early

One of the clearest demonstrations of compounding is comparing two investors — one who starts investing at age 25 and another who starts at age 35, both investing the same monthly amount until age 60.

Despite contributing for only 10 additional years, the investor who started at 25 typically ends up with a significantly larger corpus than the one who started at 35, purely because of the extra time their money had to compound.

Common Mistakes That Reduce Compounding Benefits

Withdrawing Early

Breaking an investment before its intended tenure interrupts the compounding cycle and significantly reduces the long-term benefit of staying invested.

Delaying the Start

Every year you delay starting your investment journey reduces the number of compounding periods available, which can have an outsized impact on your final corpus.

Choosing Low-Return Instruments for Long-Term Goals

Using low-return instruments for long-term goals limits the compounding effect. Matching the right instrument to your investment horizon is essential to maximise growth.

Who Benefits Most from Compound Interest?

Compound interest benefits everyone, but it has the most dramatic impact on young investors with a long time horizon ahead of them. Starting early, even with small amounts, can outperform larger investments made later in life.

Compound Interest vs Inflation

The Real Return Concept

While compound interest grows your money, inflation reduces its purchasing power over time. Your real return is the compounded growth rate minus the inflation rate.

Why This Matters

To truly build wealth, your investments need to compound at a rate higher than inflation. This is why purely safe instruments may not always be sufficient for long-term goals like retirement.

Tips to Maximise the Power of Compounding

- Start investing as early as possible, even with small amounts.

- Stay invested for the long term and avoid premature withdrawals.

- Reinvest dividends and interest instead of withdrawing them.

- Increase your investment amount gradually as your income grows.

- Choose instruments that align with your investment horizon and goals.

Conclusion

Compound interest rewards patience and consistency more than timing or large lump sums. By understanding how it works and starting your investment journey early, you give your money the maximum opportunity to grow exponentially over time.

This article is for educational purposes only and should not be considered financial advice. Consult a qualified financial professional for personalised guidance.

Explore Investro Tools

Frequently Asked Questions

Quick answers to common questions about this topic.

-

Simple interest is calculated only on the principal amount, while compound interest is calculated on the principal plus previously earned interest, leading to faster growth over time.

-

Mutual fund returns through SIPs typically compound continuously as gains are reinvested, though actual compounding depends on the fund's performance and market movements.

-

Starting early gives your money more time periods to compound, which often results in a larger corpus than investing a bigger amount for a shorter duration.

-

Yes, most fixed deposits in India compound interest quarterly, meaning interest is calculated and added to the principal every three months.