How to Save Income Tax in India: Top Strategies for Salaried Employees

For most salaried employees in India, income tax is one of the largest annual expenses. However, the Income Tax Act provides several legitimate provisions that allow you to significantly reduce your tax liability through smart planning and timely investments.

What Is Income Tax Planning?

Income tax planning is the process of organising your finances in a way that legally minimises your tax liability. It involves making use of deductions, exemptions, and rebates available under the Income Tax Act to reduce your taxable income.

Effective tax planning should ideally begin at the start of every financial year rather than at the last minute in March.

How Income Tax Is Calculated for Salaried Employees

Calculate While You Read

Free calculators related to this article — instant results, no signup.

Your tax liability is calculated on your net taxable income, which is your gross salary minus all eligible deductions and exemptions. The remaining amount is taxed according to the applicable income tax slab rates for the financial year.

Choosing between the old tax regime and the new tax regime also plays a significant role in determining your final tax outgo.

Top Ways to Save Income Tax in India

Section 80C Deductions (Up to ₹1.5 Lakh)

Section 80C is the most widely used tax-saving provision. Investments in PPF, ELSS mutual funds, life insurance premiums, NSC, tax-saving FDs, and EPF contributions all qualify for deduction up to ₹1.5 lakh per year.

Section 80CCD(1B) — NPS Additional Deduction (Up to ₹50,000)

Over and above the ₹1.5 lakh limit of Section 80C, you can claim an additional deduction of up to ₹50,000 for contributions made to the National Pension System under Section 80CCD(1B).

House Rent Allowance (HRA)

If you live in a rented house, you can claim HRA exemption on the HRA component of your salary. The exemption amount depends on your salary, actual rent paid, and the city you live in.

Standard Deduction

All salaried employees and pensioners are eligible for a flat standard deduction of ₹50,000 from their gross salary, regardless of actual expenses.

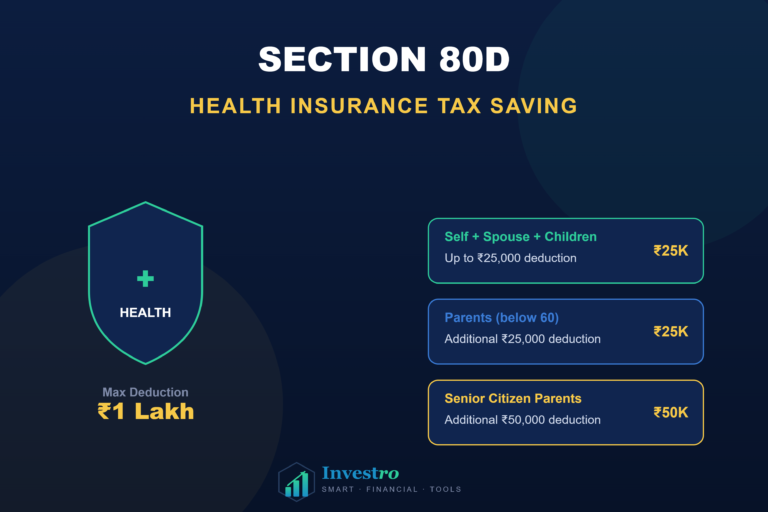

Section 80D — Health Insurance Premium

Premiums paid for health insurance for yourself, your spouse, children, and parents are eligible for deduction under Section 80D. The limit is ₹25,000 for self and family, and an additional ₹25,000 to ₹50,000 for parents depending on their age.

Home Loan Interest — Section 24(b)

If you have a home loan, you can claim a deduction of up to ₹2 lakh per year on the interest paid under Section 24(b), further reducing your taxable income.

Old Tax Regime vs New Tax Regime

Old Tax Regime

The old regime allows you to claim all deductions and exemptions mentioned above. It is generally more beneficial for individuals who have significant investments and expenses that qualify for deductions.

New Tax Regime

The new regime offers lower slab rates but removes most deductions and exemptions. It is simpler to calculate but may result in higher tax for those with substantial deductions.

Which One to Choose?

Calculate your tax liability under both regimes before making a choice. The regime that results in lower tax is the better option for your specific situation.

Common Tax Saving Mistakes to Avoid

Waiting Until March to Invest

Last-minute investments are often rushed and poorly planned. Starting early in April gives you time to choose the right instruments aligned with your financial goals.

Investing Only for Tax Saving

Many people invest in instruments solely to save tax without considering returns, liquidity, or alignment with their financial goals. Always evaluate the investment on its own merits as well.

Missing Lesser-Known Deductions

Deductions like Section 80E (education loan interest), Section 80G (charitable donations), and Leave Travel Allowance (LTA) are often overlooked but can further reduce your tax burden.

Who Should Focus on Tax Planning?

Any salaried individual with a taxable income above the basic exemption limit should actively plan their taxes. The higher your income, the greater the potential savings through proper utilisation of available deductions.

Tips for Effective Tax Planning

- Submit your investment declaration to your employer at the beginning of the financial year to avoid excess TDS deduction.

- Keep all investment proofs and receipts ready for submission to your employer by January or February.

- Use both Section 80C and Section 80CCD(1B) to maximise your deduction up to ₹2 lakh.

- Compare old and new tax regimes every year as your income and deductions may change.

- File your income tax return on time to avoid penalties and carry forward any losses.

Conclusion

Saving income tax is not about finding loopholes — it is about making the most of the provisions that the government has specifically designed to encourage saving, investment, and financial security. With the right planning, salaried employees in India can significantly reduce their annual tax burden while building long-term wealth.

This article is for educational purposes only and should not be considered financial or tax advice. Consult a qualified tax professional for personalised guidance.

Explore Investro Tools

Frequently Asked Questions

Quick answers to common questions about this topic.

-

You can save tax on investments up to ₹1.5 lakh per year under Section 80C. The actual tax saved depends on your income tax slab rate.

-

It depends on your deductions. If your total eligible deductions exceed ₹3.75 lakh, the old regime is generally more beneficial. Otherwise, the new regime may result in lower tax.

-

Salaried employees can switch between regimes every financial year when filing their ITR. However, those with business income have limited switching flexibility.

-

Tax-saving investments must be made before March 31st of the relevant financial year to be eligible for deduction in that year's tax return.