Old vs New Tax Regime: Which One Should You Choose in India?

Every year, taxpayers in India face an important decision — should they continue with the old tax regime or switch to the new one? Since both regimes follow different rules around deductions and tax slabs, choosing the right one can make a meaningful difference to your annual tax outgo.

What Are the Old and New Tax Regimes?

The old tax regime is the traditional system that allows taxpayers to claim various deductions and exemptions such as 80C, HRA, and home loan interest. The new tax regime, introduced to simplify taxation, offers lower slab rates but removes most deductions and exemptions.

Taxpayers in India can choose between the two regimes based on whichever results in a lower tax liability for their specific financial situation.

How the Two Regimes Work

Calculate While You Read

Free calculators related to this article — instant results, no signup.

Under the old regime, your taxable income is calculated after subtracting all eligible deductions from your gross income, and tax is applied on the remaining amount as per the applicable slab rates.

Under the new regime, most deductions are not available, but the income tax slabs are wider and the rates are generally lower, which can benefit taxpayers with minimal deductions.

Key Differences Between Old and New Tax Regime

Tax Slab Rates

The new regime offers lower tax rates across most income brackets, while the old regime has comparatively higher rates but allows for deduction-based reduction in taxable income.

Deductions and Exemptions

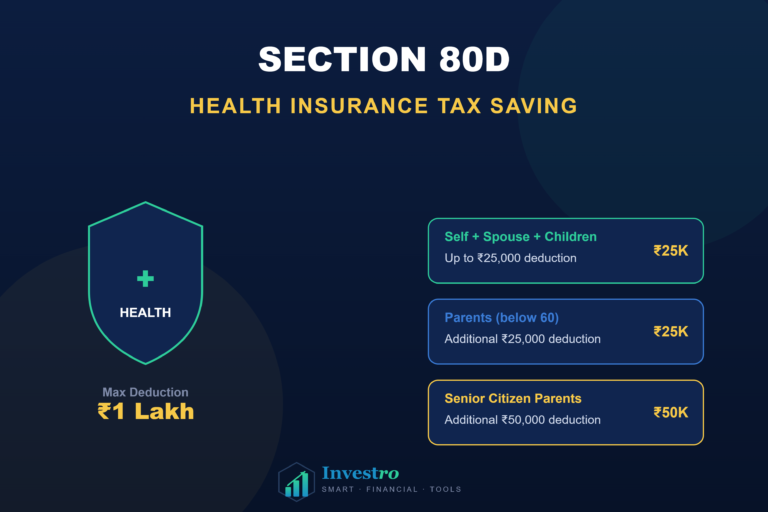

The old regime allows deductions like Section 80C, 80D, HRA, and home loan interest. The new regime removes almost all of these, except for a few specific ones like the employer’s NPS contribution.

Standard Deduction

Both regimes currently offer a standard deduction for salaried individuals and pensioners, making this one of the few common benefits across both options.

Who Benefits More from the Old Tax Regime?

The old regime is generally more beneficial for individuals who have substantial investments in tax-saving instruments, pay significant home loan interest, or claim a high HRA exemption due to living in a rented house in a metro city.

Who Benefits More from the New Tax Regime?

The new regime tends to suit individuals with fewer deductions — such as those who do not have a home loan, do not invest heavily in tax-saving instruments, or are early in their career with limited financial commitments.

How to Decide Which Regime Is Better for You

Calculate Your Tax Under Both Regimes

The most accurate way to decide is to calculate your total tax liability under both regimes using your actual income and eligible deductions, then compare the two results.

Consider Your Investment Habits

If you already invest significantly in 80C instruments, have health insurance, and pay home loan interest, the old regime may continue to offer better savings.

Account for Future Changes

If your deductions are likely to increase in the coming years — for example, if you plan to take a home loan — factor this into your decision, as it may shift the balance towards the old regime.

Advantages of the New Tax Regime

Simplicity

With fewer deductions to track and claim, tax filing becomes significantly simpler under the new regime, reducing the need for extensive documentation.

Lower Rates for Lower Deduction Claimants

Taxpayers who do not have significant deductions to claim often end up paying less tax under the new regime due to its lower slab rates.

Advantages of the Old Tax Regime

Encourages Saving and Investment

The old regime incentivises disciplined saving and investment habits through deductions tied to instruments like PPF, ELSS, and insurance.

Better for High Deduction Claimants

Individuals with home loans, high HRA, and multiple eligible deductions often find the old regime more tax-efficient despite its higher slab rates.

Can You Switch Between Regimes Every Year?

Salaried individuals with only salary income can choose between the old and new regime every financial year while filing their income tax return. However, those with business or professional income have more limited flexibility in switching regimes.

Tips for Choosing the Right Tax Regime

- List all your eligible deductions under the old regime before comparing.

- Use an online tax calculator to compute liability under both regimes accurately.

- Reassess your choice every year, especially after major financial changes like a new home loan.

- Do not choose a regime solely based on simplicity — prioritise actual tax savings.

- Consult a tax professional if your income sources are complex or include business income.

Conclusion

There is no universally better tax regime — the right choice depends entirely on your individual income, deductions, and financial habits. Calculating your tax liability under both options each year ensures you make the most tax-efficient choice for your situation.

This article is for educational purposes only and should not be considered financial or tax advice. Consult a qualified tax professional for personalised guidance.

Explore Investro Tools

Frequently Asked Questions

Quick answers to common questions about this topic.

-

Yes, salaried individuals with only salary income can choose between the two regimes every financial year while filing their income tax return.

-

Not necessarily. The new regime benefits taxpayers with fewer deductions, while those with significant deductions like home loan interest or 80C investments may save more under the old regime.

-

If you claim home loan interest deduction under Section 24(b), the old regime is often more beneficial since this deduction is not available under the new regime.

-

Yes, you should inform your employer about your preferred tax regime at the start of the financial year so that TDS is deducted accordingly from your salary.